Definition of Trend¶

The first primary cause of non-stationarity we will discuss is the presence of a trend. At its most basic level, a trend is simply a long-term increase or decrease in values.

Recall from the first chapter that time series can exhibit highly convincing spurious trends. We will cover some statistical methods to determine if a trend is real in later chapters, but none of these are fool-proof. As a data scientist, you must always combine your prior domain knowledge to assist in determining if it is reasonable to assume the existence of a trend.

Trends and Detrending¶

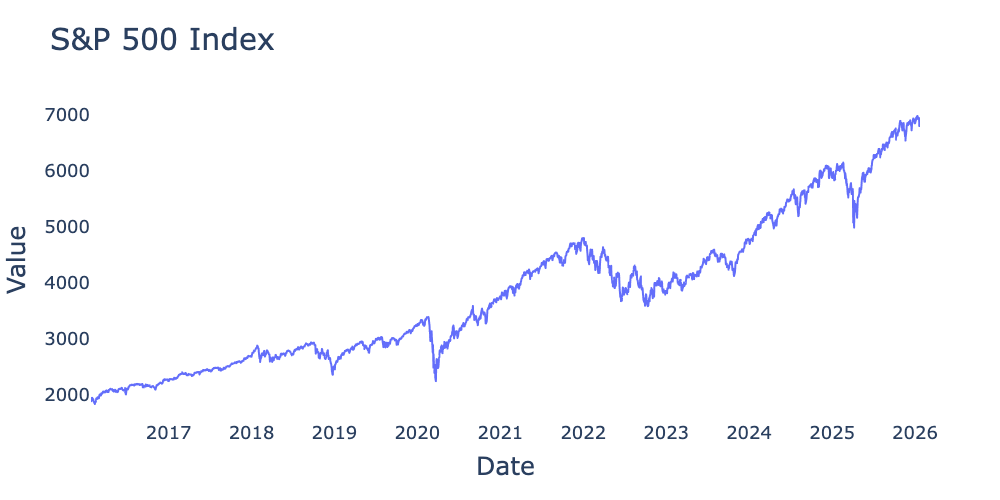

S&P 500 Trend¶

The following plot of the S&P 500 values appears to exhibit a stable overall trend.

Figure 1:Raw values of S&P 500 index for the 10-year period from January 2016 through January 2026 from Federal Reserve Bank of St. Louis.

You can experiment with the values from Figure 1 by downloading the data using the following cell:

import pandas as pd

import matplotlib.pyplot as plt

df = pd.read_csv("https://fred.stlouisfed.org/graph/fredgraph.csv?bgcolor=%23ebf3fb&chart_type=line&drp=0&fo=open%20sans&graph_bgcolor=%23ffffff&height=450&mode=fred&recession_bars=on&txtcolor=%23444444&ts=12&tts=12&width=1320&nt=0&thu=0&trc=0&show_legend=yes&show_axis_titles=yes&show_tooltip=yes&id=SP500&scale=left&cosd=2016-01-25&coed=2026-01-23&line_color=%230073e6&link_values=false&line_style=solid&mark_type=none&mw=3&lw=3&ost=-99999&oet=99999&mma=0&fml=a&fq=Daily%2C%20Close&fam=avg&fgst=lin&fgsnd=2020-02-01&line_index=1&transformation=lin&vintage_date=2026-01-25&revision_date=2026-01-25&nd=2016-01-25",

index_col=0,

parse_dates=True,

)

# statsmodels is very particular regarding missing values, we will fill in missing values with the previous value.

df.ffill(inplace=True)

# examine a quick plot

plt.plot(df)Trend Stationary Process¶

Given the apparent upward trend, it is reasonable to explore the possibility that the S&P 500 is trend stationary, i.e. the time series takes the form

where is the observed time series, is a trend, and is an underlying stationary time series. Eq. (1) suggests recovering via the process of detrending

What form should our estimate take? Let’s start with the most basic model, ordinary least squares (OLS)

where is the intercept and is the slope.

Detrending S&P 500¶

We will fit an OLS regression of the form in Eq. (3) using the following code:

import statsmodels.api as sm

import numpy as np

y = sp_500_df['SP500']

X = np.arange(len(sp_500_df))

# By default, statsmodels does not include an intercept term.

# We will add an intercept manually using add_constant.

X = sm.add_constant(X)

model = sm.OLS(y, X)

results = model.fit()

print(results.summary())You should now see something like the following:

OLS Regression Results

==============================================================================

Dep. Variable: SP500 R-squared: 0.907

Model: OLS Adj. R-squared: 0.907

Method: Least Squares F-statistic: 2.543e+04

Date: Sun, 25 Jan 2026 Prob (F-statistic): 0.00

Time: 18:33:02 Log-Likelihood: -19337.

No. Observations: 2610 AIC: 3.868e+04

Df Residuals: 2608 BIC: 3.869e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1644.6932 15.634 105.199 0.000 1614.037 1675.350

x1 1.6550 0.010 159.469 0.000 1.635 1.675

==============================================================================

Omnibus: 10.728 Durbin-Watson: 0.011

Prob(Omnibus): 0.005 Jarque-Bera (JB): 10.076

Skew: -0.117 Prob(JB): 0.00649

Kurtosis: 2.806 Cond. No. 3.01e+03

==============================================================================Note that the is quite high, and both the intercept and slope are statistically significant.

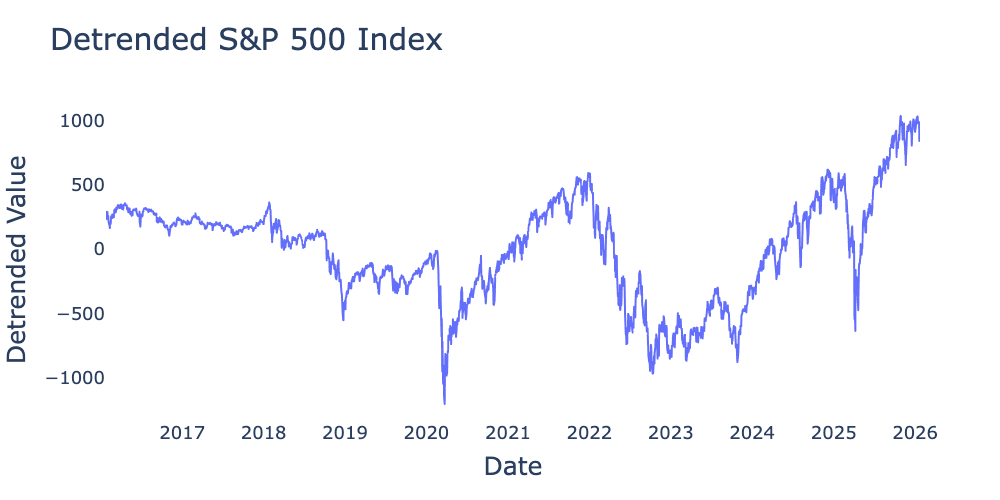

Based on the results of our OLS, we will detrend the S&P 500 results using the formula

where consists of for observations. We can apply this formula using the code

detrend_component = results.params["const"] + results.params["x1"] * np.arange(len(sp_500_df))

sp_500_df_detrended = sp_500_df["SP500"] - pd.Series(detrend_component, index=sp_500_df.index)

Figure 2:Detrended values of S&P 500 index for the 10-year period from January 2016 through January 2026 from Federal Reserve Bank of St. Louis detrended using .